On the Constitutional and Operational Incoherence of the Strategic Bitcoin Reserve

The Constitutional Observer

24 min read

The Constitutional Observer

24 min read

I. Introduction

On 6 March 2025, the President of the United States signed Executive Order 14233, “Establishment of the Strategic Bitcoin Reserve and United States Digital Asset Stockpile,” published five days later in the Federal Register. See Exec. Order No. 14233, 90 Fed. Reg. 11789 (Mar. 11, 2025). The Order directs the Secretary of the Treasury to capitalise a “Strategic Bitcoin Reserve” with all bitcoin (BTC) “finally forfeited” to the federal government, declares that “Government BTC deposited into the Strategic Bitcoin Reserve shall not be sold,” and instructs the Secretaries of Treasury and Commerce to develop “budget-neutral” strategies for further acquisition. Id. § 3. The Order rests, on its face, “on the authority vested in [the President] as President by the Constitution and the laws of the United States of America.” Id. preamble. It identifies no specific statutory base.

The Order’s rhetorical premise — repeated in its first section — is that bitcoin is “digital gold,” and that “there is a strategic advantage to being among the first nations to create a strategic bitcoin reserve.” Id. § 1. The premise is intuitive and intuitively wrong. The instrument the Order proposes to treasure cannot, by deliberate engineering, do what monetary reserves are kept to do; the authority by which the Order proposes to do it cannot, by the architecture of Article I, perform what the Order attempts; and the analogy by which the Order disarms criticism — the analogy to gold — operates, on examination, against the Order’s conclusion rather than for it. The thesis of this essay is that the Strategic Bitcoin Reserve is constitutionally and operationally incoherent on three independent grounds, each of which is sufficient to refuse it serious credit.

The first ground is constitutional, and is the subject of Parts III and IV. The monetary power of the United States is vested in Congress under the Coinage Clause, U.S. Const. art. I, § 8, cl. 5, and is plenary in Congress within the limits the Court has marked out. Juilliard v. Greenman, 110 U.S. 421 (1884). The President has no general monetary power and may not legislate one into being by executive order. The Appropriations Clause, U.S. Const. art. I, § 9, cl. 7, further forbids the unilateral re-direction of property and money in the Treasury away from statutorily authorised uses. Off. of Pers. Mgmt. v. Richmond, 496 U.S. 414 (1990). The seized and forfeited bitcoin which the Order proposes to immobilise indefinitely is, by statute, allocable to specified law-enforcement purposes. 31 U.S.C. § 9705. The Order does not — because it cannot — repeal those provisions.

The second ground is operational, and is the subject of Parts V and VI. A reserve asset must, at the minimum, be able either to discharge the obligations it backs or to be exchanged into instruments that can. Gold has done this for five thousand years. Bitcoin Core cannot. Its protocol is capped at approximately five transactions per second across the entire global network — a ceiling that defines the system rather than a bottleneck inviting optimisation. A “reserve” of an asset whose throughput cannot service the transactional volume of the sovereign that holds it is not, on any historically grounded definition, a reserve. It is a position in a thinly tradable commodity that the holder is forbidden by its own protocol to use.

The third ground is structural and is the burden of Part VII. The Order conflates two distinct functions — the settlement function performed by base monetary assets and the circulating function performed by claims redeemable into them — and in doing so reproduces, in software, the architecture of correspondent banking the digital-cash literature claimed to abolish. The Reserve is a reserve of nothing in particular, backing nothing in particular, settled against nothing in particular. It is rhetorical.

The argument proceeds in seven parts. Part II sets out what Executive Order 14233 does and does not do. Part III treats the Coinage and Legal Tender powers and locates Bitcoin Core within them. Part IV addresses the Appropriations Clause and the disposition of forfeited assets. Part V compares the gold reserve regime under the Gold Reserve Act of 1934 and concludes that the comparison favours the critic. Part VI explains why the five-transactions-per-second throughput cap is not merely a technical inconvenience but a structural defeat of the reserve thesis. Part VII addresses the deeper incoherence — a reserve of what, against what claim, in what stack — and Part VIII concludes.

II. What Executive Order 14233 Does

The text of the Order is short. It establishes two distinct entities. The Strategic Bitcoin Reserve is to consist of “Government BTC” — defined as bitcoin held by the Treasury that “was finally forfeited as part of criminal or civil asset forfeiture proceedings or in satisfaction of any civil money penalty imposed by any executive department or agency” and that “is not needed to satisfy requirements under 31 U.S.C. 9705 or released pursuant to subsection (d).” Exec. Order No. 14233, § 3(a). The United States Digital Asset Stockpile is the parallel account for non-bitcoin digital assets. Id. § 3(b).

Three operative provisions matter. First, all BTC currently held by federal agencies as a result of forfeiture must be reviewed for transfer to the Reserve within thirty days. Id. § 3(a). Second, “Government BTC deposited into the Strategic Bitcoin Reserve shall not be sold and shall be maintained as reserve assets of the United States utilized to meet governmental objectives.” Id. Third, the Secretaries of Treasury and Commerce are directed to “develop strategies for acquiring additional Government BTC provided that such strategies are budget-neutral and do not impose incremental costs on United States taxpayers.” Id. § 3(c). The Order purports to leave existing statutory authority undisturbed: “Nothing in this order shall be construed to impair or otherwise affect: (i) the authority granted by law to an executive department or agency, or the head thereof . . . .” Id. § 5(a).

Three features of this design are worth observing at the outset. The first is the no-sell rule. The Order converts what would otherwise be a transitional holding — assets seized and forfeited, awaiting disposition under the Treasury Forfeiture Fund mechanism — into permanent custody. The Treasury Forfeiture Fund Act, 31 U.S.C. § 9705, contemplates that forfeited assets be either disposed of and the proceeds applied to law-enforcement expenditures, victim remission, equitable sharing, and the other purposes the statute prescribes, or held only as administratively necessary for those statutorily defined ends. The no-sell rule is not a continuation of the statutory regime. It is a unilateral suspension of it.

The second feature is the “budget-neutral” qualifier. The Order does not direct the Treasury to spend appropriated funds to acquire bitcoin. It cannot. To do so would draw on the Treasury without appropriation in plain violation of Article I, § 9, cl. 7. The Order’s drafters appear to understand this. They restrict the acquisition strategy to revenue-neutral methods — presumably revaluation of existing gold certificates, sale or swap of other digital assets in the Stockpile, or use of revenue-generating mechanisms outside the appropriations cycle. Each of these methods raises its own statutory and constitutional questions, examined in Part IV.

The third feature is the absence of statutory citation. The Order does not invoke any specific Act of Congress as the source of its authority — only “the Constitution and the laws of the United States” in the abstract. By contrast, the analogous gold provisions in 1933 and 1934 — Executive Order 6102 (Apr. 5, 1933), and the Gold Reserve Act of 1934, ch. 6, 48 Stat. 337 — proceeded under express statutory authority (the Trading with the Enemy Act of 1917 as amended by the Emergency Banking Act of 1933, ch. 1, 48 Stat. 1) and Congressional enactment respectively. The absence of any equivalent legislative architecture in 2025 is the structural complaint developed below.

III. The Coinage Power, the Legal Tender Power, and Who Holds Them

Article I, § 8, clause 5 of the Constitution provides that “The Congress shall have Power . . . To coin Money, regulate the Value thereof, and of foreign Coin, and fix the Standard of Weights and Measures.” Clause 2 of the same section vests in Congress the power “To borrow Money on the credit of the United States.” The Coinage Clause was written against a background in which the Articles of Confederation had given Congress (and the states) overlapping monetary authority, with predictably ruinous results. See Bray Hammond, Banks and Politics in America from the Revolution to the Civil War 89–91 (1957). The Framers responded by federalising the coinage power and forbidding the states from making “any Thing but gold and silver Coin a Tender in Payment of Debts.” U.S. Const. art. I, § 10, cl. 1; see The Federalist No. 44 (Madison) (treating state currency emissions as the disease the Clause was written to cure).

The textual lodging of the monetary power in Congress is reinforced by an unbroken doctrinal history. In McCulloch v. Maryland, 17 U.S. (4 Wheat.) 316 (1819), Chief Justice Marshall established that Congress’s enumerated powers carry with them the implied authority to choose appropriate means — including monetary instruments — for their execution. The Legal Tender Cases following the Civil War tested how far that implication extended. In Hepburn v. Griswold, 75 U.S. (8 Wall.) 603 (1870), a divided Court initially held that Congress could not make Treasury notes legal tender for pre-existing private debts. The decision was overruled within a year. Knox v. Lee, 79 U.S. (12 Wall.) 457 (1871). A decade later, the Court placed the question beyond doubt: Congress’s power to make the notes of the United States legal tender extends to peacetime as well as wartime, and is “implied from the express power to borrow money on the credit of the United States.” Juilliard v. Greenman, 110 U.S. 421, 437–50 (1884).

The Gold Clause Cases of 1935 ratified this consolidation in still stronger terms. In Norman v. Baltimore & Ohio Railroad Co., 294 U.S. 240 (1935), the Court — Hughes, C.J., writing for the majority — upheld the Joint Resolution of June 5, 1933, which had abrogated private gold clauses, on the ground that Congress’s authority to regulate the currency reaches private contractual provisions that would frustrate the monetary policy validly adopted by Congress. Id. at 302–11. In Perry v. United States, 294 U.S. 330 (1935), the Court found, more narrowly, that while the abrogation of gold clauses in government bonds was beyond Congress’s power, no plaintiff had suffered cognisable damages. Id. at 357–58. Justice McReynolds’s dissent, joined by Justices Van Devanter, Sutherland, and Butler, registered the obvious — that the majority had effectively sanctioned a sovereign default through the device of damages doctrine — but the majority’s view that the monetary power is plenary in Congress was not seriously contested even by the dissenters. See generally John P. Dawson, The Gold Clause Decisions, 33 Mich. L. Rev. 647 (1935); Kenneth W. Dam, The Legal Tender Cases, 1981 Sup. Ct. Rev. 367.

Two propositions follow from this body of law, and they bear on the Order. First, the monetary power is Congressional, not Presidential. The President has no Article II authority to declare an asset a monetary reserve of the United States in any sense that would impose duties on the Treasury or alter the statutory regime governing forfeited property. The Order’s failure to cite specific statutory authority is not an oversight; it is the necessary result of the architecture of Article I. Second, Congress’s monetary power, while plenary, has been treated as extending to instruments Congress itself has authorised: Treasury notes, Federal Reserve notes, the gold and silver coinage. Compare 31 U.S.C. § 5103 (designating United States coins and currency, including Federal Reserve notes, as legal tender) with the absence of any statute designating BTC for any monetary function. Bitcoin is not “coined” by Congress, not denominated in dollars, not issued by or backed by any organ of the United States, and not declared legal tender by any Act.

This is not, taken alone, a constitutional defect. The United States Treasury holds many assets that are neither coined nor legal tender — including, today, approximately 261.5 million troy ounces of gold, valued on Treasury books at the statutory rate of $42.2222 per ounce. See 31 U.S.C. § 5117(b). What it is, however, is a clarification of the limited domain within which the Order can plausibly operate. The Order cannot declare BTC a monetary instrument of the United States; it can only attempt to direct that existing holdings be retained rather than disposed of. Whether the President possesses even that more modest authority — given the statutory regime governing forfeiture — is the question of Part IV.

IV. The Appropriations Clause and the Disposition of Forfeited Assets

The Appropriations Clause is the most straightforward of the constitutional problems and the least often noticed in the policy commentary on the Order. Article I, § 9, clause 7 provides: “No Money shall be drawn from the Treasury, but in Consequence of Appropriations made by Law.” The clause is, in form, a limitation on executive action rather than an enumeration of legislative power. Its function is to assure that public funds will be spent according to the judgments reached by Congress as to the common good and not according to the discretion of executive officers. Off. of Pers. Mgmt. v. Richmond, 496 U.S. 414, 427–28 (1990).

The Clause’s reach is broad. As the Court explained in Richmond, “[a]ny exercise of a power granted by the Constitution to one of the other branches of Government is limited by a valid reservation of congressional control over funds in the Treasury.” Id. at 425. The Court drew an analytical line from Justice Story’s treatment of the Clause as a “useful and salutary check upon profusion and extravagance, as well as upon corrupt influence and public peculation,” 2 Joseph Story, Commentaries on the Constitution of the United States § 1348 (3d ed. 1858) (cited at 496 U.S. at 427), through Reeside v. Walker, 52 U.S. (11 How.) 272 (1851), and Knote v. United States, 95 U.S. 149 (1877), to the more recent confirmation in Maine Community Health Options v. United States, 140 S. Ct. 1308 (2020). The line is unambiguous. Funds in the Treasury may be drawn only as Congress directs.

The Treasury Forfeiture Fund Act of 1992, codified as amended at 31 U.S.C. § 9705, is one such direction. Pub. L. No. 102-393, tit. VI, § 638, 106 Stat. 1779 (Oct. 6, 1992) (originally codified at 31 U.S.C. § 9703; renumbered § 9705 by Pub. L. No. 114-22, § 105(c)(1)(A), 129 Stat. 237 (2015)). The statute creates a special fund in the Treasury, deposits to which are made from non-tax forfeitures effected under laws administered by Treasury enforcement agencies. Subsection (a) enumerates the purposes for which the Fund’s resources are “available to the Secretary, without fiscal year limitation”: payment of expenses of seizure and forfeiture proceedings, payments to informers under the Tariff Act of 1930, satisfaction of valid liens and mortgages, equitable sharing with state and local law-enforcement entities, and the various ancillary law-enforcement expenditures the statute specifies. 31 U.S.C. § 9705(a)(1)–(2). A parallel regime under the Department of Justice Assets Forfeiture Fund, 28 U.S.C. § 524(c), governs forfeitures administered by Justice agencies. Together, these provisions form a comprehensive statutory architecture for the disposition of forfeited property — including, on any reasonable reading, forfeited bitcoin.

The Order’s no-sell rule sits awkwardly with this architecture. The Order does not direct that BTC be sold to fund the statutorily prescribed law-enforcement purposes; nor does it direct that BTC be sold to satisfy victim restitution obligations, equitable sharing, or any of the other statutorily authorised uses of forfeited property. It directs, instead, that BTC “shall not be sold.” This is not a continuation of the statutory regime by other means. It is an exemption from the regime, effected by executive instruction, in respect of one specific asset class. The Order’s saving clause — “Nothing in this order shall be construed to impair or otherwise affect: (i) the authority granted by law to an executive department or agency,” Exec. Order No. 14233, § 5(a) — is the kind of clause that often appears in executive orders precisely where the instrument is open to the charge that it overrides existing law. Its presence does not resolve the question; it announces that the drafters anticipated it.

The doctrinal framework for evaluating such a conflict is Justice Jackson’s tripartite analysis in Youngstown Sheet & Tube Co. v. Sawyer, 343 U.S. 579, 635–38 (1952) (Jackson, J., concurring). Where the President acts pursuant to express or implied authorisation of Congress, his authority is at its maximum. Where Congress has neither granted nor denied authority, the President acts in a “zone of twilight.” Where the President takes measures incompatible with the expressed or implied will of Congress, his power is at its “lowest ebb,” and his action will be sustained only if Congress’s own constitutional power on the subject is unavailing or absent. Id.

The Order does not fit comfortably in Category One. There is no Act of Congress authorising the President to establish a Strategic Bitcoin Reserve, to suspend the statutory regime for forfeited assets in respect of BTC, or to direct that forfeited BTC be held indefinitely without disposition. The Order’s preamble cites only the Constitution and “the laws of the United States” generally — a formulation that signals the absence of specific statutory authority rather than its presence.

The Order is closer to Category Three than to Category Two. The Treasury Forfeiture Fund Act, 31 U.S.C. § 9705, expresses a statutory will: forfeited assets (other than the tax-related ones expressly excluded) are to be available to the Secretary for the enumerated law-enforcement purposes. The no-sell rule withdraws BTC from that statutory regime. It is not “incompatible” with the statute on a narrow reading — the statute does not require sale within any particular time-frame, and Treasury has historically held forfeited cryptocurrency for varying periods. But the indefinite retention of a forfeited asset specifically to serve a new purpose (national reserve accumulation) for which Congress has not authorised any expenditure or programme is a measure that operates beside, rather than within, the statutory scheme. The Train v. City of New York, 420 U.S. 35 (1975), problem looms: an executive may not impound funds that Congress has directed to be applied to a statutory purpose. Whether the analogy is exact depends on facts not yet developed in litigation, but it is no longer fanciful.

Then there is the acquisition question. The Order’s “budget-neutral” qualifier confines further BTC acquisition to revenue-neutral mechanisms. The only such mechanisms compatible with existing law are limited and contested. Revaluation of the Treasury’s gold certificates above the statutory price of $42.2222 per ounce — 31 U.S.C. § 5117(b) — would require Congressional action; the statutory rate has not been touched since the Par Value Modification Act of 1972, Pub. L. No. 92-268, 86 Stat. 116. Sales from the Digital Asset Stockpile to purchase BTC for the Reserve would convert one category of forfeited asset into another, with the constitutional and statutory questions multiplied rather than resolved. The “budget-neutral” qualifier is itself a tacit recognition that direct appropriation would be required for an honest acquisition strategy, and that no such appropriation has been made.

Whether the Order is, in the strict legal sense, ultra vires is a question on which a court would have to be persuaded by an injured plaintiff with standing, a question of remedy, and a measure of the Treasury Secretary’s discretion under 31 U.S.C. § 9705. None of these conditions is met today and none may ever be. The constitutional defect, however, is independent of justiciability. An executive order which directs the indefinite retention of property statutorily allocated to specified law-enforcement purposes, without Congressional authorisation, sits on weak constitutional ground regardless of whether anyone is positioned to say so in court.

V. The Gold Reserve Analogue, Properly Drawn

The Order’s first section likens BTC to “digital gold” and argues that a strategic reserve in BTC is the modern analogue of a national reserve in bullion. The comparison is misplaced in two distinct ways.

First, the gold reserve regime was Congressional, not executive. Executive Order 6102 of April 5, 1933, which required the surrender of gold coin, bullion, and gold certificates, did not invent its own authority. It operated under the Trading with the Enemy Act of 1917, ch. 106, 40 Stat. 411, as amended by the Emergency Banking Act of 1933, ch. 1, 48 Stat. 1 — an Act passed by Congress on March 9, 1933, three days into Roosevelt’s presidency. The Gold Reserve Act of 1934, ch. 6, 48 Stat. 337 (codified as amended in scattered sections of 31 U.S.C.), then transferred title to the nation’s monetary gold to the United States, authorised the President to fix the dollar’s gold content (within Congressionally specified bounds), established the Exchange Stabilization Fund, and prescribed how the Treasury’s gold would be handled thereafter. See Milton Friedman & Anna J. Schwartz, A Monetary History of the United States, 1867–1960, at 463–72 (1963) (recounting the legislative architecture of the 1933–34 measures). The Court’s eventual approval of the gold programme in the Gold Clause Cases proceeded entirely on the basis of Congress’s plenary monetary power, not on any free-standing executive authority. Norman, 294 U.S. at 302–04, 307–11; Perry, 294 U.S. at 350–53.

The constitutional architecture of 2025, set against this, is impoverished. The Strategic Bitcoin Reserve is established by executive order without underlying enabling legislation. There is no Bitcoin Reserve Act. There is no statute authorising the Treasury to hold cryptocurrency as a permanent national reserve. There is no statute fixing the terms on which BTC may be acquired, held, valued, sold, or used to discharge any obligation. The Order operates in a statutory vacuum that the gold regime never inhabited, and the absence of an enabling Act is a constitutional weakness the Order’s “budget-neutral” qualifier silently concedes.

Second, the asset itself differs in the precise respect that the analogy requires it not to. Gold’s reserve status is grounded in two characteristics. It is a physical commodity with a verifiable mass and purity that has been the subject of a deep institutional infrastructure — assayers, mints, custodial vaults, central-bank cooperation, the London bullion market, the COMEX delivery system — for centuries. See Charles A. E. Goodhart, The Evolution of Central Banks 102–19 (1988). And its value has been stable, in long-run real terms, in a manner that BTC’s historical annualised volatility makes a mockery of. A reserve asset that loses or gains half its dollar value in a year is not, by any usable definition of the word, a reserve. It is a position. The Treasury’s gold has not behaved that way. BTC has done so repeatedly.

The historical comparison thus cuts in the opposite direction from the one the Order’s drafters appear to assume. Gold was a successful reserve because Congress legislated the regime, because the asset had a centuries-old institutional architecture supporting its monetary use, and because its value behaved over decades in ways that admitted of being relied upon. BTC has none of these features. The Order’s invocation of the gold analogy as authority for what it does is, on examination, an invocation of the very precedent that defeats it.

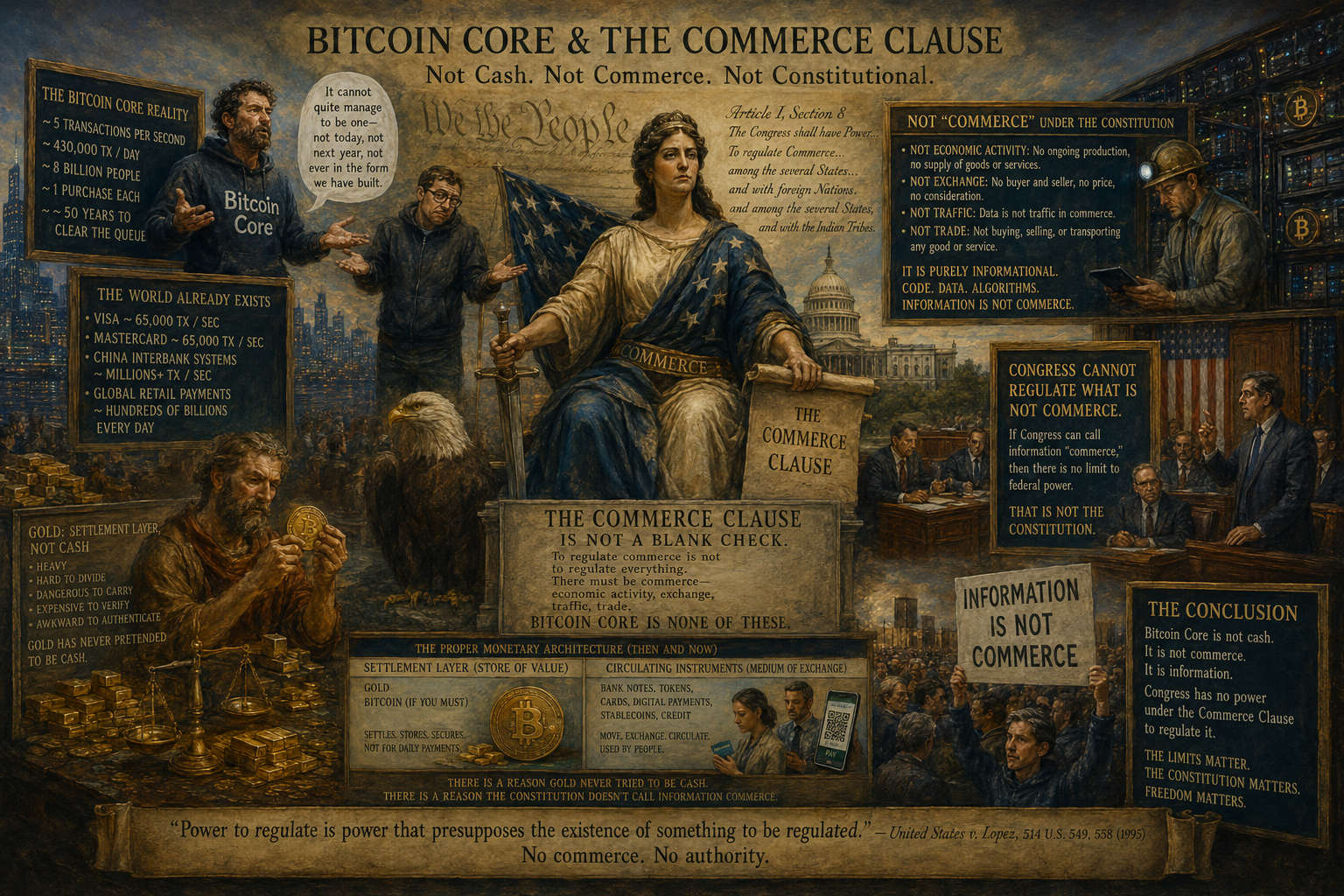

VI. Five Transactions a Second: Why the Throughput Cap Is a Constitutional Problem

This is the section the technical literature has, with few exceptions, declined to write. The Bitcoin Core protocol’s throughput is bounded, by deliberate design, at a level somewhere between three and seven transactions per second across the entire global network — a figure commonly given as five and used here for convenience. The bound arises from the conjunction of three engineering choices: the average ten-minute interval between blocks, the approximately one-megabyte base block size (with witness data accommodated through the Segregated Witness discount), and the absence of any horizontal-scaling mechanism within the base protocol. The constraint is not a bottleneck inviting optimisation. It is the system. The system was designed this way, has been kept this way, and is defended on first-principle grounds by the developers and proponents of the chain.

Why does throughput bear on the constitutional analysis? In two ways, each independently sufficient.

First, the Coinage and Legal Tender powers presuppose an instrument capable of performing the functions of money. The history of the Legal Tender Cases is consistent on this. The Treasury notes upheld in Knox v. Lee and Juilliard v. Greenman were instruments that could circulate at the volumes the United States economy demanded; the Federal Reserve notes upheld in subsequent jurisprudence were, similarly, capable of bearing the transactional load of a continental economy. The monetary power of Congress is not a power to declare arbitrary objects “money”; it is, on the doctrinal record, a power to authorise instruments that can perform monetary functions. An asset whose protocol-imposed throughput is mathematically incapable of supporting the transactional volume of even a mid-sized retail chain on a busy afternoon is not, on any operationally meaningful definition, a candidate for the monetary functions Congress’s power was framed to authorise. The point is not that Congress could not, by Act, designate BTC for some balance-sheet purpose; the point is that the doctrinal grounding for treating a particular asset as “money” in the legal-tender sense has, historically, presupposed a capacity the asset does not have. See Carl Menger, On the Origins of Money, 2 Econ. J. 239 (1892) (on the saleability conditions a commodity must satisfy to attain monetary function).

Set the numbers down. Visa’s network processes peak loads in the order of 65,000 transactions per second, with sustained capacity well above that; Mastercard, the Chinese interbank settlement systems, and the regional ACH equivalents move comparable volumes. United States retail payment volume is in the hundreds of millions of transactions per day on the credit and debit rails alone. The Bitcoin Core network, at five transactions per second, settles approximately 432,000 transactions per day across the world. If every adult in the United States — roughly 260 million people — sought to make a single purchase on the chain, the queue would take approximately 600 days to clear, assuming no other use of the network in the interim. The figures do not improve materially under any defensible doubling or trebling of throughput.

Second, and more directly relevant to the Order, a reserve asset’s reserve function is to back claims that circulate. The historical structure of every functioning commodity-money regime — and the gold regime under which the Treasury’s bullion reserves operate today — depends on the base asset being able, in principle and at the necessary volume, to discharge the obligations that reference it. The Treasury’s gold can be sold, delivered, swapped, or revalued at any volume the financial system requires. It is held precisely because it can perform these functions when called upon. BTC cannot. The base layer is throughput-capped at five per second. The notional gold-and-notes hierarchy reconstructed in software — base-layer BTC settled occasionally; Lightning Network channels, custodial exchange balances, and stablecoins serving the circulating role — places the supposed reserve asset in a position where it cannot, by protocol, discharge the obligations of the circulating layer at any meaningful fraction of its current notional volume. A reserve that cannot service its own claims is not a reserve in any operational sense. It is a balance-sheet entry whose meaning is contingent on no one acting on it.

The empirical record on the chain’s stress behaviour confirms what the arithmetic predicts. During the fee-market episodes of late 2017, the spring of 2021, and the ordinal-inscription periods of 2023, mempool congestion drove transaction fees from cents to figures regularly exceeding fifty dollars per transaction. These were minor demand shocks against a network already operating near its design capacity. The fees were not the price signal of an efficient market clearing demand against supply; they were the auction price of a scarce inclusion right, conducted against a fixed and binding block-space ceiling. A reserve asset whose redemption mechanism becomes an auction priced at hundreds of dollars per transaction the moment it is asked to perform at scale is, in plain language, not exchangeable. Inexchangeability is incompatible with reserve function.

There is a tertiary consequence, which the security-budget literature has begun to address. Bitcoin Core’s long-run security depends on the combination of the block subsidy (declining on a deterministic halving schedule toward zero) and transaction fees. The throughput cap binds the fee base. The system therefore confronts a long-run tension: it requires fee revenue to grow to compensate for the falling subsidy, but its design forbids the volume of fee-generating activity that would permit fees to grow without choking the use that generates them. A reserve asset whose long-run security guarantees rest on the unresolved exit from this tension is an asset whose suitability for reserve status is open to a question more serious than the holders typically concede.

VII. A Reserve of What? Structural Incoherence

The deeper incoherence is conceptual. Reserves, in the orthodox monetary architecture, occupy a definite position in a hierarchy of instruments. The base reserve — historically gold, today a portfolio of foreign exchange, gold, and special drawing rights — backs claims that circulate. The claims are denominated in the unit of account (the dollar) and are convertible into the base asset under specified conditions. The hierarchy is structural and explicit. See Hammond, supra, at 1–15 (treating the bank-note-as-claim structure of nineteenth-century American banking).

Where does BTC fit in this hierarchy? It is not the unit of account. The Reserve is denominated, on Treasury books, in dollars; the BTC are valued in dollars at market prices. It is not legal tender. 31 U.S.C. § 5103 designates U.S. coin and currency for that function, and contains no provision for BTC. It is not redeemable into anything else by the Treasury. The Order does not establish a redemption mechanism, a peg, or any operational link between BTC holdings and any obligation the Treasury owes. It is, in the precise sense the orthodox literature would use, an asset on the balance sheet — like the gold, but unlike the gold in not being backed by an enabling statute that prescribes its functional role.

If the BTC is not money, not a claim, and not a backing instrument for any specifically identified claim, what is it doing on the Treasury’s balance sheet? The Order’s own answer is unsatisfactory. Section 1 invokes the strategic-advantage rhetoric — being “among the first nations to create a strategic bitcoin reserve” — but this is a marketing statement, not a monetary or fiscal proposition. The instrument is held because holding it is said to be advantageous, without specification of the channel through which the advantage operates.

Compare the gold position. The Treasury’s gold serves at least three identifiable functions: it backs gold certificates issued to the Federal Reserve Banks (31 U.S.C. § 5117(b)); it stands as a residual asset against the foreign-exchange operations of the Exchange Stabilization Fund; and it provides an emergency reserve in extremis, mobilisable under statute. Each of these is a specific function, attached to a specific statutory and operational architecture. The gold is not merely “held”; it is held against identifiable obligations and operational contingencies.

The Strategic Bitcoin Reserve has no analogous architecture. It is held against no obligations. Its acquisition is “budget-neutral” — that is, not funded by Congressional appropriation — and its disposition is forbidden by the no-sell rule. It is, structurally, a one-way valve: assets enter, no assets exit, and no use of the assets while held is contemplated by the Order. This is not a reserve in the orthodox sense. It is an inventory.

The conceptual problem deepens when one asks what the Reserve backs. If the answer is “nothing in particular,” then the Reserve is, at best, a speculative position in a particular cryptocurrency at the expense of the statutorily directed disposition of forfeited assets. If the answer is “the dollar’s long-term stability,” the proposition is novel, untested, and incompatible with the existing dollar reserve regime, which rests on gold, foreign exchange, and SDRs in a portfolio configured for tested macro-financial functions. If the answer is “future fiscal capacity,” then the Reserve is a speculative asset whose value is bet on appreciation — a proposition that converts the United States Treasury, by executive instruction, into a directional position in a single cryptocurrency in violation of every conventional principle of sovereign asset management. Whichever construction is preferred, the result is either trivial or unsound.

Beneath the structural incoherence sits the reality the Order’s first sentence concedes and the rest of the Order obscures: BTC is, on the proponents’ own description, “digital gold.” Gold sits at the base of a hierarchy in which it backs circulating claims it does not itself perform. The same architecture, reproduced for BTC, would place the chain at the base and require Lightning Network channels, custodial exchange balances, stablecoins, and other secondary instruments to serve the circulating role. None of these is the chain. None is held by the Treasury. The Reserve is therefore a reserve of a base-layer asset for a circulation layer the United States does not own, operate, or control. The architecture the Order proposes is the architecture of correspondent banking with the correspondents replaced by exchanges and the cash replaced by stablecoins, and the United States Treasury holding the gold that backs a system it does not regulate.

VIII. Conclusion

Each of the three grounds developed above is sufficient on its own. Together they are dispositive. The Strategic Bitcoin Reserve is constitutionally infirm because the President lacks the unilateral authority to direct the indefinite retention of forfeited assets in violation of the statutory regime governing their disposition, and because the Appropriations Clause forecloses unilateral acquisition by any method not Congressionally authorised. It is operationally unworkable because the asset’s throughput ceiling makes it incapable of performing the monetary functions a reserve asset is held to support. It is structurally incoherent because the Order establishes a reserve of an asset against no specified obligation, with no redemption mechanism, no enabling Act, and no analogue in the gold regime to which the Order rhetorically appeals.

The choice before the Congress, if it cares to address what the Order has begun, is therefore narrow. Either it passes a Bitcoin Reserve Act that prescribes the Reserve’s funding, governance, acquisition criteria, disposition rules, and operational functions — placing the regime, as the gold regime was placed in 1934, within the architecture of Article I — or it permits the Reserve to continue as an executive curiosity whose constitutional foundations are weak and whose operational basis is, on inspection, fictitious. The former path is available. The Trading with the Enemy Act / Gold Reserve Act sequence of 1933–34 is the historical template. The latter path will produce, in the fullness of time, the kind of litigation in which the constitutional defects sketched above will be examined by parties less polite than the present author.

There is a further consideration, on the operational side, that the foregoing has not pressed. The Order treats BTC as “digital gold.” It is not. Gold, for all the limits the prior essay on this Substack identified, is closer to cash than BTC, because gold can be physically transferred in arbitrary amounts without protocol approval, settles instantly at the point of transfer, and is supported by a centuries-deep institutional architecture for verification, custody, and exchange. BTC cannot match any of these properties at the volumes a sovereign reserve would, in extremis, be called upon to demonstrate. The asset the Order proposes to treasure is, by deliberate design, less monetarily useful than the metal it claims to replicate. The chain has not improved on gold; it has reproduced gold’s limits without gold’s compensating institutional depth.

The Strategic Bitcoin Reserve is therefore neither what its drafters claim nor what the Constitution permits the President alone to create. It is an executive gesture toward an asset whose technical architecture forecloses the function the gesture invokes, founded on an authority the gesture does not possess, governed by a no-sell rule that operates beside rather than within the statutory regime for forfeited property, and acquired by methods that cannot be made constitutional without the legislation the Order conspicuously declines to seek. The proper response is not partisan. It is institutional. Congress should legislate the regime, or the Executive should rescind the Order. The status quo is a constitutional embarrassment supported by a technical impossibility, and time will not improve either condition.

References

Constitutional Provisions. U.S. Const. art. I, § 8, cls. 2, 5, 18; art. I, § 9, cl. 7; art. I, § 10, cl. 1; art. II, § 3; amend. V.

Cases. McCulloch v. Maryland, 17 U.S. (4 Wheat.) 316 (1819); Reeside v. Walker, 52 U.S. (11 How.) 272 (1851); Hepburn v. Griswold, 75 U.S. (8 Wall.) 603 (1870); Knox v. Lee (Legal Tender Cases), 79 U.S. (12 Wall.) 457 (1871); Knote v. United States, 95 U.S. 149 (1877); Juilliard v. Greenman, 110 U.S. 421 (1884); Norman v. Baltimore & Ohio R.R. Co., 294 U.S. 240 (1935); Nortz v. United States, 294 U.S. 317 (1935); Perry v. United States, 294 U.S. 330 (1935); Youngstown Sheet & Tube Co. v. Sawyer, 343 U.S. 579 (1952); Train v. City of New York, 420 U.S. 35 (1975); Off. of Pers. Mgmt. v. Richmond, 496 U.S. 414 (1990); Me. Cmty. Health Options v. United States, 140 S. Ct. 1308 (2020).

Statutes and Executive Documents. Coinage Act of 1792, ch. 16, 1 Stat. 246; Trading with the Enemy Act of 1917, ch. 106, 40 Stat. 411; Emergency Banking Act of 1933, ch. 1, 48 Stat. 1; Gold Reserve Act of 1934, ch. 6, 48 Stat. 337; Treasury Forfeiture Fund Act of 1992, Pub. L. No. 102-393, tit. VI, § 638, 106 Stat. 1779 (codified as amended at 31 U.S.C. § 9705); 28 U.S.C. § 524(c); 31 U.S.C. § 5103; 31 U.S.C. § 5117; Par Value Modification Act of 1972, Pub. L. No. 92-268, 86 Stat. 116; Exec. Order No. 6102 (Apr. 5, 1933); Exec. Order No. 14233, 90 Fed. Reg. 11789 (Mar. 11, 2025).

Secondary Sources. The Federalist Nos. 30 (Hamilton), 44 (Madison); 2 Joseph Story, Commentaries on the Constitution of the United States (3d ed. 1858); Bray Hammond, Banks and Politics in America from the Revolution to the Civil War (1957); John P. Dawson, The Gold Clause Decisions, 33 Mich. L. Rev. 647 (1935); Milton Friedman & Anna J. Schwartz, A Monetary History of the United States, 1867–1960 (1963); Carl Menger, On the Origins of Money, 2 Econ. J. 239 (1892); Kenneth W. Dam, The Legal Tender Cases, 1981 Sup. Ct. Rev. 367; Charles A. E. Goodhart, The Evolution of Central Banks (1988).