Labour, Capital, and Constitutional Error: Why Proof-of-Work and Proof-of-Stake Cannot Be Regulated as One

The Constitutional Observer

8 min read

The Constitutional Observer

8 min read

A Doctrinal Analysis of Consensus Mechanisms Under U.S. Securities, Tax, and Administrative Law.

There are moments in legal development when a category error, left unchallenged, metastasizes into doctrine. It begins innocently enough—with regulators faced by novelty, commentators seduced by simplification, and policymakers eager for a framework that can be applied with minimal intellectual exertion. Over time, however, the convenience calcifies. Distinctions are blurred, then erased, and what was once confusion becomes orthodoxy.

The present treatment of blockchain consensus mechanisms in United States law stands precisely at that precipice.

Proof-of-work and proof-of-stake—two systems frequently invoked in the same breath—are, in prevailing regulatory discourse, treated as though they were merely variations of a single phenomenon. They are analysed under the same securities frameworks, taxed under the same assumptions, and subjected to the same conceptual apparatus. This is not merely imprecise. It is wrong in a way that produces cascading legal consequences.

The argument advanced here is neither radical nor speculative. It is, in fact, doctrinally conservative. Proof-of-work is service provision. Proof-of-stake is capital deployment. The former falls naturally within the domain of labour and business activity. The latter aligns, in both structure and effect, with equity and yield-bearing instruments. To collapse these into a single regulatory category is to misapply foundational principles of U.S. law, particularly under the Securities Act of 1933, the Internal Revenue Code, and the Administrative Procedure Act.

What is remarkable is not that the distinction exists. It is that it has been so persistently ignored.

I. The Ontological Question: Participation as Service Versus Participation as Ownership

Legal classification begins, or ought to begin, with ontology. What is the nature of the activity being regulated? What is the relationship between the participant and the system?

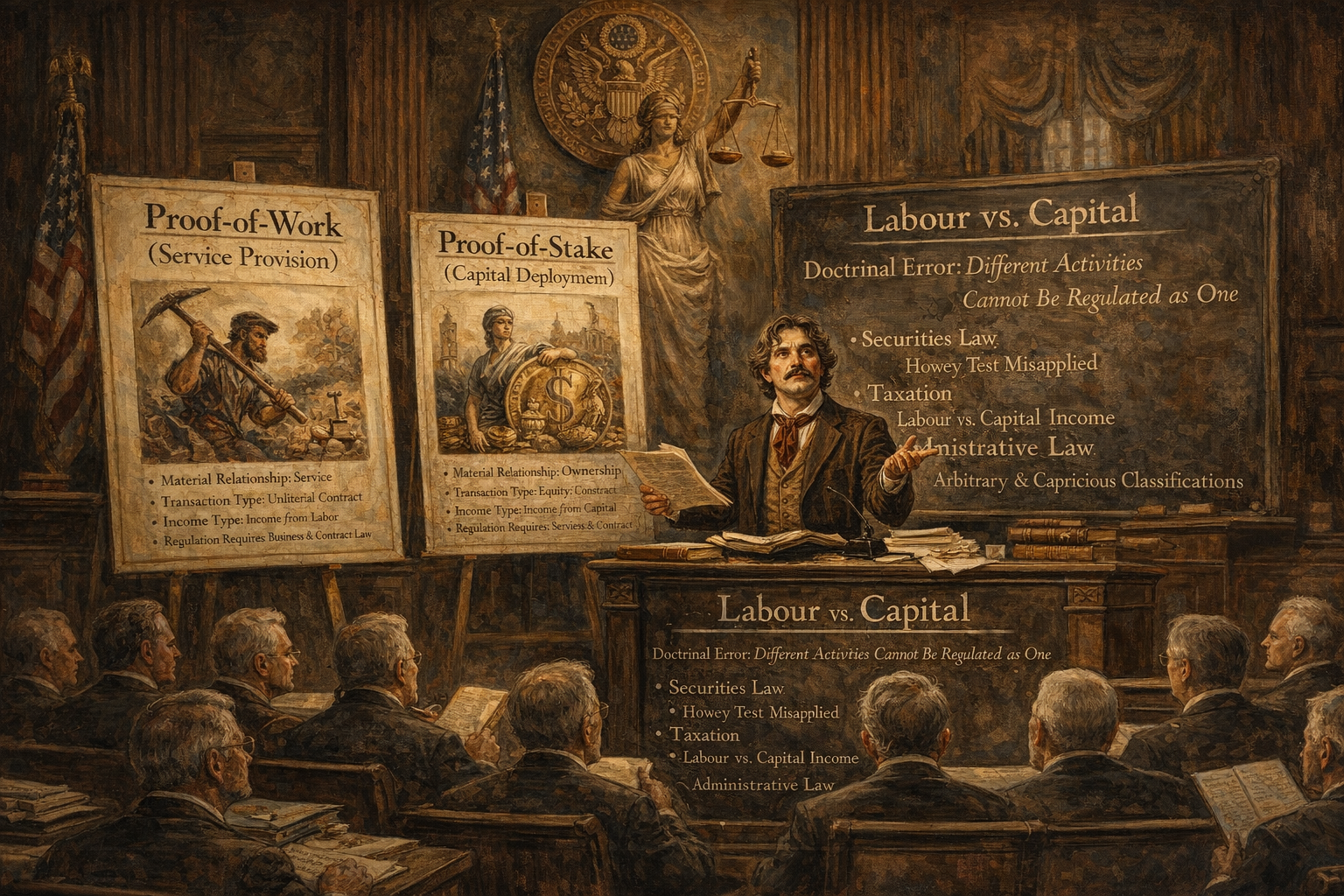

In proof-of-work systems, the participant—conventionally termed a miner—engages in a competitive process of computational validation. The miner expends energy, deploys hardware, and performs a discrete, verifiable task. Compensation is contingent upon success. No ownership of the underlying digital asset is required to participate. One may mine without holding any tokens at all.

This is not an investment. It is a service.

The structure is readily recognisable within contract law. The protocol offers what is, in effect, a unilateral contract: perform a specified task (solve a valid hash), and receive a defined reward. The miner accepts by performance. Consider Carlill v. Carbolic Smoke Ball Co. (1893), the canonical unilateral contract case. The offer is made to the world; the reward is earned by completion. The analogy is exact.

Proof-of-stake systems invert this relationship.

Here, participation is conditioned upon ownership. One must hold and commit the native asset—staking it as collateral—in order to validate. Rewards accrue in proportion to the amount staked. The validator’s return is not contingent upon discrete acts of labour but upon the maintenance of capital within the system.

This is not service. It is ownership deployed to generate yield.

The distinction is not semantic. It is structural. In proof-of-work, the participant stands external to the asset and interacts with it instrumentally. In proof-of-stake, the participant is internal to the asset; the act of validation is inseparable from possession.

American law has long recognised the difference between earning through action and earning through ownership. The failure to apply that recognition here is not a deficiency of doctrine, but of its application.

II. Securities Law: The Howey Test Misapplied

The central inquiry in U.S. securities law remains the test articulated in SEC v. W.J. Howey Co., 328 U.S. 293 (1946). The elements are well known: an investment of money in a common enterprise with an expectation of profits derived from the efforts of others.

Applied correctly, the test yields divergent results for proof-of-work and proof-of-stake.

A. Proof-of-Work: No Investment Contract

Proof-of-work mining does not satisfy the Howey criteria.

First, there is no investment of money in a common enterprise. The miner purchases equipment and electricity, but these are inputs into a productive activity, not contributions to a shared venture. The miner competes against others rather than pooling resources with them.

Second, the expectation of profit is not derived from the efforts of others. The miner’s return is the direct consequence of his own computational work. The protocol does not manage capital; it merely enforces rules.

Third, there is no reliance on managerial or entrepreneurial efforts of a promoter. The system is rule-based and deterministic. Success is a function of performance, not delegation.

The SEC has, notably, refrained from treating proof-of-work mining as a securities activity per se. This restraint, whether deliberate or incidental, reflects an implicit recognition of the underlying distinction.

To classify mining as a security would be to expand Howey beyond recognition, capturing within its ambit any activity involving expenditure with the hope of return. Such an interpretation would collapse the distinction between investment and enterprise.

B. Proof-of-Stake: The Investment Analogy

Proof-of-stake, however, presents a markedly different profile.

The participant commits capital—the staked tokens—to the system. The return is proportional to that capital and accrues over time. Critically, the return depends not solely on the participant’s own actions, but on the continued functioning and integrity of the network, including the efforts of developers, validators, and users.

The structure bears a resemblance to traditional investment arrangements, particularly when staking is conducted through intermediaries.

Consider staking-as-a-service providers. They pool customer assets, manage validation operations, and distribute returns. The participant contributes capital, delegates management, and receives proportional yield. This is, in substance, indistinguishable from a managed investment vehicle.

The SEC’s enforcement actions against such arrangements suggest an intuitive alignment with Howey, even where the doctrinal articulation remains incomplete.

The critical point is this: proof-of-stake introduces the very elements that proof-of-work lacks—capital commitment, proportional return, and reliance on the system’s collective operation.

To treat both identically is to misapply the test at the level of first principles.

III. Taxation: Income from Labour Versus Income from Capital

The Internal Revenue Code distinguishes, often with painful specificity, between income derived from services and income derived from capital.

This distinction is not merely classificatory. It affects rates, deductions, timing, and reporting obligations.

A. Proof-of-Work: Business Income

Mining rewards are properly classified as income from services or business activity.

The miner incurs costs—electricity, hardware depreciation, facilities—and receives compensation for performing a task. Under § 61 of the Code, gross income includes all income from whatever source derived, including compensation for services. The miner’s activities fall squarely within this category.

Deductions under § 162 for ordinary and necessary business expenses apply. The economic structure aligns with that of a contractor or producer.

There is no conceptual difficulty here.

B. Proof-of-Stake: Capital Income

Staking rewards, by contrast, arise from the deployment of capital.

The staker commits an asset and receives a return proportional to that commitment. The analogy is not to wages, but to dividends or interest. The asset itself is productive.

This raises complex questions of timing—when is income realised?—and character—should it be treated as ordinary income or capital gain? But the underlying classification is clear: the source of the income is ownership, not labour.

Failure to recognise this distinction produces distortions.

If staking rewards are treated as service income, participants may face inappropriate tax burdens, misaligned incentives, and compliance uncertainty. Conversely, treating mining rewards as capital income would allow deductions and timing benefits that are inconsistent with their economic substance.

The law already possesses the tools to distinguish these categories. It need only use them.

IV. Financial Regulation: Collective Investment Schemes and Delegation

The regulatory treatment of pooled arrangements further illustrates the divergence.

In proof-of-stake systems, staking pools aggregate capital from multiple participants. The pool operator performs validation, manages technical operations, and distributes rewards. Participants contribute assets and receive proportional returns.

This structure aligns closely with the concept of a collective investment scheme.

While U.S. law does not use that exact terminology, analogous concepts exist under the Investment Company Act of 1940 and related regulatory frameworks. The pooling of capital, delegation of management, and proportional distribution of returns are hallmarks of regulated investment entities.

Proof-of-work pools differ fundamentally.

Participants contribute computational power, not capital. The pool coordinates effort but does not manage assets. Rewards are distributed based on contributed work, not ownership stake.

The analogy is not to an investment fund, but to a cooperative or partnership of service providers.

To regulate both under the same framework is to ignore the nature of the contributions being aggregated.

V. Administrative Law: Arbitrary and Capricious Classification

The failure to distinguish between proof-of-work and proof-of-stake raises questions under the Administrative Procedure Act.

Agency action that is arbitrary, capricious, or not in accordance with law is subject to judicial review. A regulatory framework that treats materially distinct activities as identical, without reasoned explanation, risks falling within this category.

The Supreme Court’s jurisprudence, from Motor Vehicle Manufacturers Ass’n v. State Farm (1983) onward, requires agencies to engage in reasoned decision-making. They must consider relevant factors and articulate a rational connection between facts and conclusions.

Applying identical treatment to service provision and capital deployment, without acknowledging their differences, fails this standard.

It is not sufficient to invoke technological novelty as a justification for doctrinal imprecision. The law has encountered novelty before. Its strength lies in its capacity to classify, not its willingness to generalise.

VI. Constitutional Implications: Due Process and Economic Liberty

At a deeper level, the misclassification of consensus mechanisms implicates constitutional principles.

Due process requires that legal obligations be defined with sufficient clarity to allow individuals to conform their conduct. A regime that fails to distinguish between fundamentally different activities introduces uncertainty that may rise to the level of constitutional concern.

Moreover, the regulation of economic activity engages longstanding principles of liberty, even within the deferential framework of modern jurisprudence.

To impose securities regulation on service providers, or to deny appropriate classification to capital deployment, is to interfere with economic arrangements in a manner that must, at the very least, be justified.

The Constitution does not demand perfect classification. It does, however, require that the classifications adopted bear a rational relationship to reality.

VII. The Case for Differentiation

The conclusion is, by this point, unavoidable.

Proof-of-work and proof-of-stake are not variants of a single category. They are distinct legal phenomena. One is labour-based, competitive, and external. The other is capital-based, proportional, and internal.

The appropriate regulatory response is not to invent new categories, but to apply existing ones correctly.

Proof-of-work should be treated as business activity. Proof-of-stake should be analysed, with appropriate nuance, as capital deployment, with particular attention to arrangements that resemble securities or investment schemes.

This is not a call for deregulation or overregulation. It is a call for accurate regulation.

VIII. A Note on Blind Review and the Occasional Triumph of Merit

It is, perhaps, worth observing—if only with a measure of restrained amusement—that these arguments have been accepted for presentation following blind peer review.

There is something almost theatrical in the process. Names are removed, reputations set aside, and the work is evaluated on its content alone. One might even say it approximates an ideal rarely achieved elsewhere.

In this instance, the result has been gratifying.

The paper was accepted. It will be presented. It will, in due course, be published. And it will enter the broader conversation, where it will encounter all the usual forces—agreement, resistance, misunderstanding, and the occasional moment of clarity.

One is tempted to conclude that anonymity has its advantages.

IX. Conclusion

Legal systems do not fail for lack of complexity. They fail for lack of precision.

The classification of consensus mechanisms is not a peripheral issue. It sits at the intersection of securities law, taxation, and financial regulation. It determines rights, obligations, and risks. It shapes the evolution of an entire technological domain.

To treat proof-of-work and proof-of-stake as identical is to build that domain on a faulty foundation.

The correction is straightforward. The consequences, however, are significant.

And that, perhaps, is why it has taken so long to make it.